First Look: Personal Finance Software--the 2007 Lineup

Yardena Arar, PC World

Quicken 2007 sports a new look, while Microsoft introduces a simplified version of Money for new users.

The 2007 versions of the two big packages in personal finance software, Intuit Quicken and Microsoft Money, will be on retail shelves this month, but don't feel obligated to race to the computer store (online or otherwise) to buy a copy of either one. I tried out a late beta version of Quicken Premier 2007 and shipping copies of Money 2007 Premium and the new Money Essentials; and though some features looked good, I saw nothing that made me wildly enthusiastic.

Don't get me wrong--I use personal finance software and wouldn't do without it. But it's pretty underwhelming when the main reason you'd advise someone to upgrade is to maintain the support for online services that both Microsoft and Intuit withdraw from users of older versions of their products. Intuit is slightly better on this score than Microsoft: It makes you upgrade Quicken only once every three years, while Microsoft ends online services support after just two years for most versions of Money. The exception is Money Essentials--Microsoft limits its online services for that program to a single year.

It's the first of several skimpy aspects of Essentials, which the company created in hopes of enticing people who currently use Web-based banking services but who have thus far found desktop financial managers too intimidating or too expensive. (You can't import existing Money data into Essentials, so only new users need apply.) At $20, Essentials is certainly cheap, but it's so lacking in features that some newcomers may wonder what the fuss over desktop software is all about.

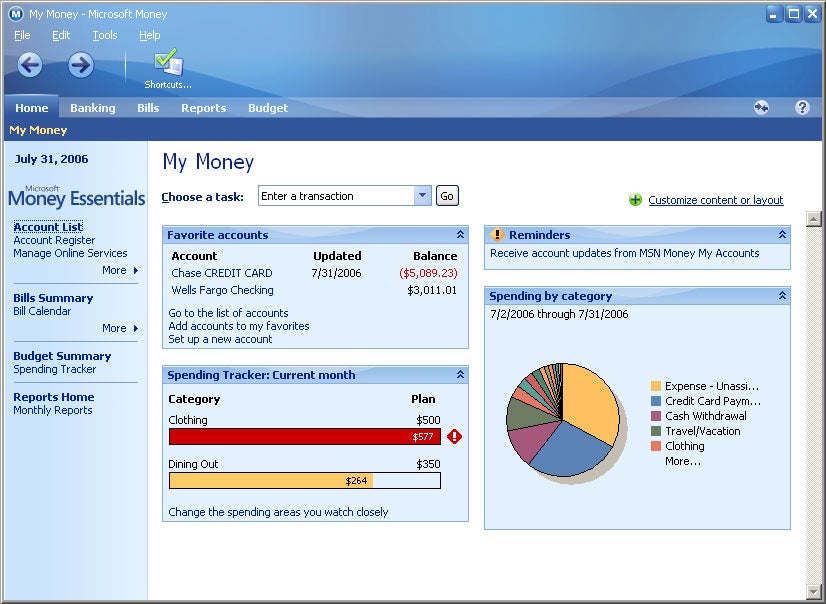

Bare-Bones Finance TrackingAs its name suggests, Essentials does provide the basics: You can download transaction data from most banks and assign basic categories in order to track spending and income. You can also enter monthly bills and track which ones you've paid. And you can export data to tax preparation software that supports the .txf file format, including TaxCut and TurboTax. Microsoft's interface is pleasing, too, with its colorful spending pie chart and trackers that let you see whether you're adhering to spending limits that you specify for up to three categories of your choice.

Bare-Bones Finance TrackingAs its name suggests, Essentials does provide the basics: You can download transaction data from most banks and assign basic categories in order to track spending and income. You can also enter monthly bills and track which ones you've paid. And you can export data to tax preparation software that supports the .txf file format, including TaxCut and TurboTax. Microsoft's interface is pleasing, too, with its colorful spending pie chart and trackers that let you see whether you're adhering to spending limits that you specify for up to three categories of your choice.

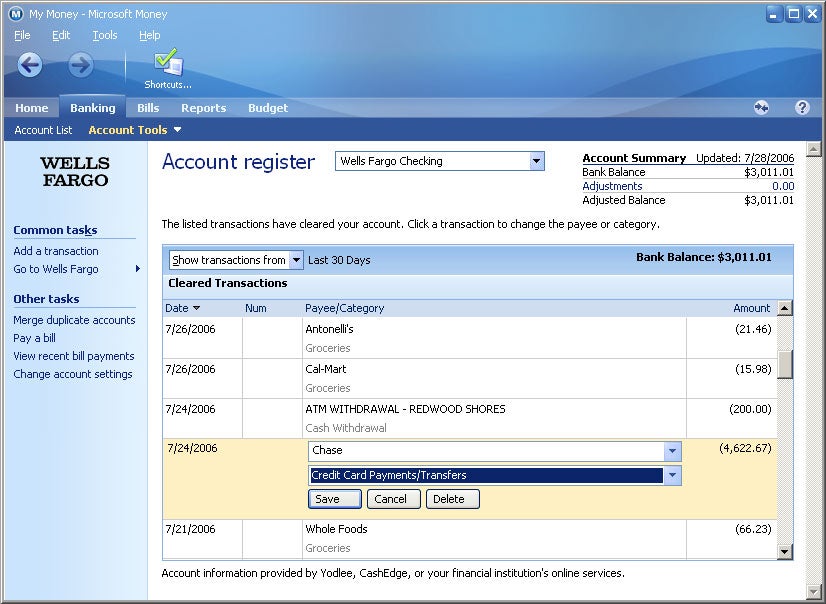

But the account registers provide no field for notes to help you remember details of specific transactions (what concert did that Ticketmaster charge pay for?). And there's no support for transfer transactions: If you record a payment to Visa in your checking account, it won't show up in the register for that Visa account unless you enter it manually or download it from Visa. Furthermore, you can't divide a transaction between multiple categories. If you go shopping at Costco, for example, you can't assign part of the expense to groceries and part to clothing.

Not surprisingly, Essentials doesn't offer any of the investment and planning features that other versions of Money (to varying degrees) provide. For $20, I wouldn't expect it to.

But Microsoft hasn't revealed how much it will charge for online service support beyond the included year. People interested in desktop software might be better off investing in the $50 Deluxe version of Money (Microsoft offers a $20 mail-in rebate) and getting two years of support plus a tool they can grow into.

Both Microsoft and Intuit have done a good job of simplifying the new-user setup in their products to accommodate impatient customers. If you don't want to enter account data right away, simply skip to the home page. As a result of this improvement, there's less reason than ever to get a dumbed-down package.

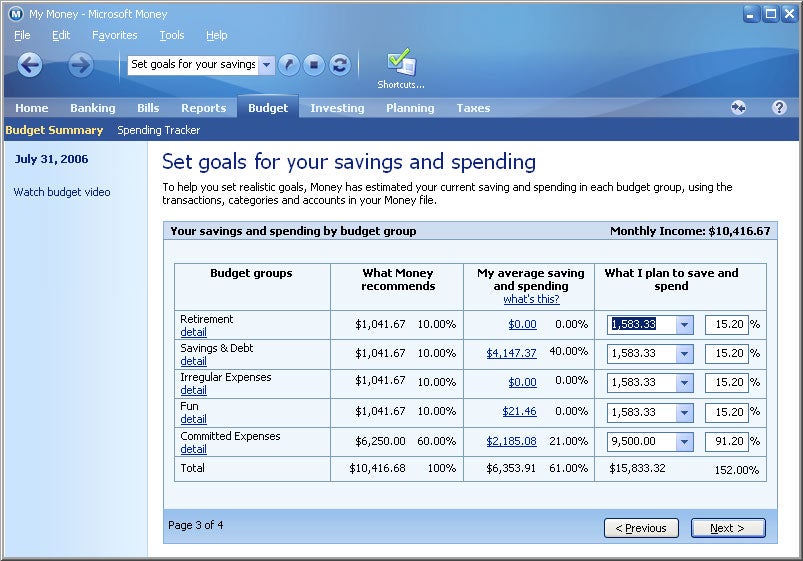

Full-Featured OptionsThe biggest innovation in Microsoft's full-featured Premium edition this year is a budgeting tool based on a strategy for building savings developed by MSN Money editor-in-chief Richard Jenkins. In an article (available in the software) called "A Simpler Way to Save: The 60% Solution," Jenkins recommends allocating 60 percent of your gross income for what he calls "committed expenses"--food, clothing, household essentials, insurance, charitable contributions, regular bills, and taxes. That leaves 10 percent for retirement savings, 10 percent for long-term savings, 10 percent for irregular expenses (read: emergencies), and 10 percent for "fun money"--basically anything else.

Money's budgeting feature provides a calculator for the plan, though you can adjust the percentages to suit your fancy. If you're going to upgrade, the plan calculator might be worth trying, but I wouldn't recommend upgrading just to get this feature. The same goes for other (and smaller) new features; by and large, they're simply tweaks of existing ones.

Money's modular and customizable user interface covers all the basics. But Money is still missing a great feature that Intuit introduced in Quicken last year: the ability to attach electronic records. And until Microsoft adds that (and matches Quicken's three-year support for online services), Intuit will continue to hold the edge.

The 2007 versions of the two big packages in personal finance software, Intuit Quicken and Microsoft Money, will be on retail shelves this month, but don't feel obligated to race to the computer store (online or otherwise) to buy a copy of either one. I tried out a late beta version of Quicken Premier 2007 and shipping copies of Money 2007 Premium and the new Money Essentials; and though some features looked good, I saw nothing that made me wildly enthusiastic.

Don't get me wrong--I use personal finance software and wouldn't do without it. But it's pretty underwhelming when the main reason you'd advise someone to upgrade is to maintain the support for online services that both Microsoft and Intuit withdraw from users of older versions of their products. Intuit is slightly better on this score than Microsoft: It makes you upgrade Quicken only once every three years, while Microsoft ends online services support after just two years for most versions of Money. The exception is Money Essentials--Microsoft limits its online services for that program to a single year.

It's the first of several skimpy aspects of Essentials, which the company created in hopes of enticing people who currently use Web-based banking services but who have thus far found desktop financial managers too intimidating or too expensive. (You can't import existing Money data into Essentials, so only new users need apply.) At $20, Essentials is certainly cheap, but it's so lacking in features that some newcomers may wonder what the fuss over desktop software is all about.

Bare-Bones Finance TrackingAs its name suggests, Essentials does provide the basics: You can download transaction data from most banks and assign basic categories in order to track spending and income. You can also enter monthly bills and track which ones you've paid. And you can export data to tax preparation software that supports the .txf file format, including TaxCut and TurboTax. Microsoft's interface is pleasing, too, with its colorful spending pie chart and trackers that let you see whether you're adhering to spending limits that you specify for up to three categories of your choice.But the account registers provide no field for notes to help you remember details of specific transactions (what concert did that Ticketmaster charge pay for?). And there's no support for transfer transactions: If you record a payment to Visa in your checking account, it won't show up in the register for that Visa account unless you enter it manually or download it from Visa. Furthermore, you can't divide a transaction between multiple categories. If you go shopping at Costco, for example, you can't assign part of the expense to groceries and part to clothing.

Not surprisingly, Essentials doesn't offer any of the investment and planning features that other versions of Money (to varying degrees) provide. For $20, I wouldn't expect it to.

But Microsoft hasn't revealed how much it will charge for online service support beyond the included year. People interested in desktop software might be better off investing in the $50 Deluxe version of Money (Microsoft offers a $20 mail-in rebate) and getting two years of support plus a tool they can grow into.

Both Microsoft and Intuit have done a good job of simplifying the new-user setup in their products to accommodate impatient customers. If you don't want to enter account data right away, simply skip to the home page. As a result of this improvement, there's less reason than ever to get a dumbed-down package.

Full-Featured OptionsThe biggest innovation in Microsoft's full-featured Premium edition this year is a budgeting tool based on a strategy for building savings developed by MSN Money editor-in-chief Richard Jenkins. In an article (available in the software) called "A Simpler Way to Save: The 60% Solution," Jenkins recommends allocating 60 percent of your gross income for what he calls "committed expenses"--food, clothing, household essentials, insurance, charitable contributions, regular bills, and taxes. That leaves 10 percent for retirement savings, 10 percent for long-term savings, 10 percent for irregular expenses (read: emergencies), and 10 percent for "fun money"--basically anything else.

Money's budgeting feature provides a calculator for the plan, though you can adjust the percentages to suit your fancy. If you're going to upgrade, the plan calculator might be worth trying, but I wouldn't recommend upgrading just to get this feature. The same goes for other (and smaller) new features; by and large, they're simply tweaks of existing ones.

Money's modular and customizable user interface covers all the basics. But Money is still missing a great feature that Intuit introduced in Quicken last year: the ability to attach electronic records. And until Microsoft adds that (and matches Quicken's three-year support for online services), Intuit will continue to hold the edge.

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment